Improving Challenger Bank Metrics with Phone-Centric Identity™

While a better banking experience has been the mantra for challenger banks, diversity in operating models and customer journeys specific to target segments pose barriers to their growth.

Challenger banks have been the poster boys of innovation in the banking industry over the last decade. Research by Exton Consulting says that there are over 250 challenger banks globally. With a sharp focus on solving fundamental problems in peoples’ financial lives, a user experience that matches popular social apps, and superior customer service, challenger banks have positively disrupted legacy banking. The accelerated adoption of digital services brought about by COVID-19 has further provided a shot-in-the-arm for their growth. Some of the largest challenger banks in the world, such as WeBank, Nubank, Chime, N26, and Revolut, have several million users.

Challenger banks vary by target segment and operating model. For example, Nubank targets the financial inclusion segment in Brazil, Chime gives advance access to one’s paycheck, Greenlight caters to kids and teens, and Judo Bank in Australia provides SME-specific banking services. At the same time, some challenger banks operate under regulatory licenses (such as Monzo and Starling Bank in the UK), whereas some like Chime partner with licensed incumbents.

Hurdles in Scaling Business

While a better banking experience has been the mantra for challenger banks, diversity in operating models and customer journeys specific to target segments pose barriers to their growth. Here are three of the top challenges faced by challenger banks in the course of their growth:

Sustained User Growth: Apart from marketing spend, a better onboarding experience also dictates user growth. Regardless of the operating model, funnel conversion has heavy dependencies on legislated KYC, AML & identity checks, fraud checks, the time & effort required for form-filling, and the number of keystrokes. This study by Built For Mars shows how challenger banks in the UK trump incumbents in customer onboarding metrics such as fewer clicks and lesser questions.

Although far superior to incumbents in onboarding experience, it is a constant challenge and pursuit for challenger banks to continuously improve their origination experience to corner more of the market share.

Lower Customer Acquisition Cost (CAC) and Higher Lifetime Value (LTV): Several studies show that the average cost of customer acquisition for challenger banks is in the range of $25 to $50. Although fractional compared to an average of $200 to $300 for incumbents, market pressures to drive towards profitability and sustainability have put the spotlight on CAC. At the same time, the focus on customer retention has also become a critical consideration to improving LTV. This requires continuously improving user experience, ease of operation, unparalleled customer service, and better products and services—all of which lead to a higher customer wallet share.

Better Security: With exponential growth in cyber fraud since the onset of the pandemic, there is a critical need to improve security by fortifying existing authentication methods and processes. However, reinforcing security should not happen at the expense of user experience and convenience.

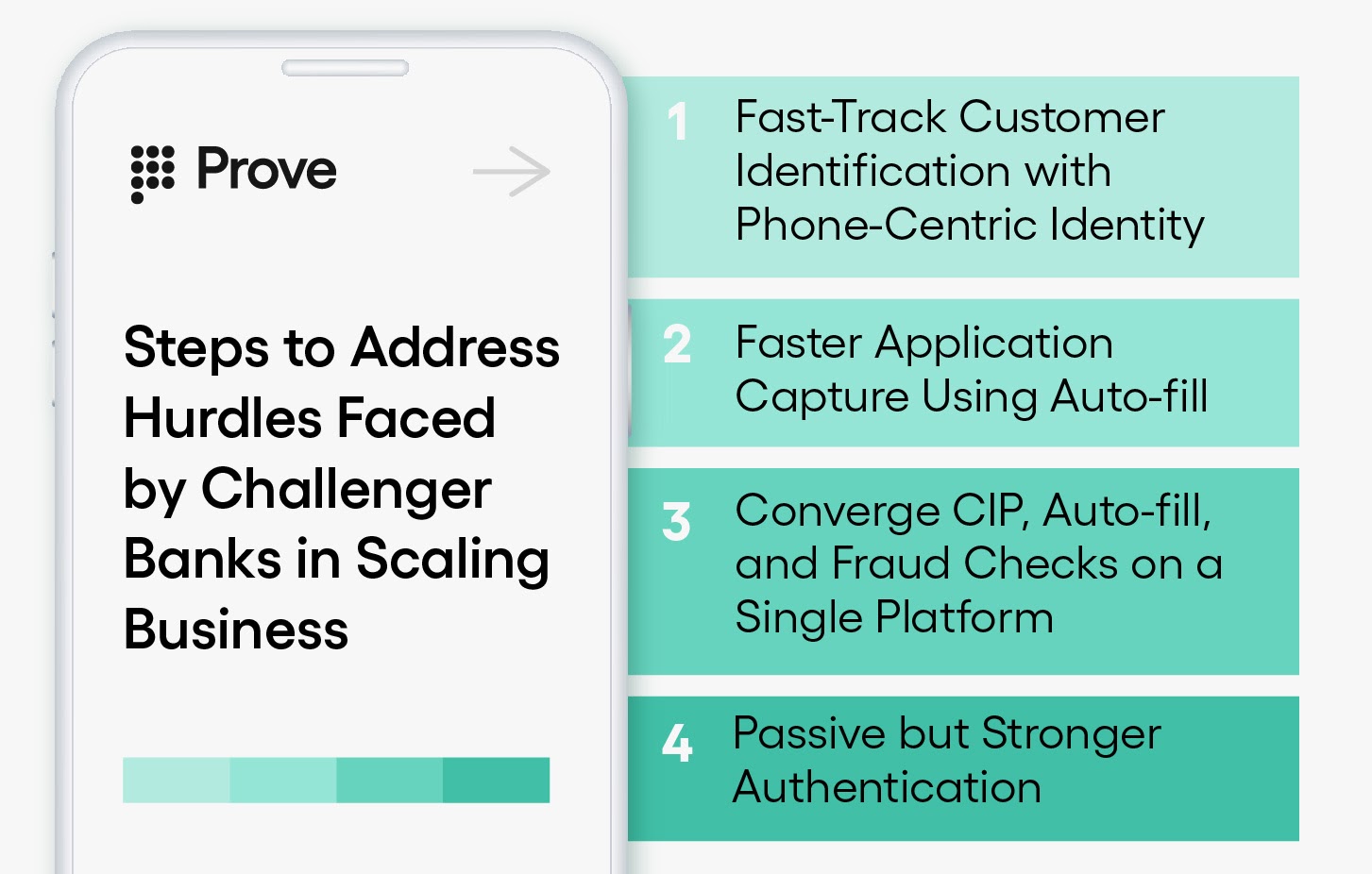

Steps to Address These Hurdles

Fast-Track Customer Identification with Phone-Centric Identity: Currently, Customer Identification Procedures (CIP) rely on traditional, legacy identity databases for identity verification and authentication. However, identity fragmentation across multiple data sources—both public and private—is a serious barrier to performing foolproof KYC. While legacy identity verification methods rely on traditional identifiers, modern methods call for using the phone number as a unique identifier due to its omnipresent nature and the richness of intelligence it provides by potentially connecting to a diverse set of data sources.

With higher confidence levels in the validation output (optionally strengthened by a risk score), Phone-Centric Identity verification improves straight through and routes fewer applications into manual verification queues. The result is better SLAs, faster onboarding, and better conversion from prospects to customers.

Prove’s Identity Verify™ supports electronic identity verification for KYC. Designed to be consumed as a simple API, Identity Verify leverages authorized data sources and matches the phone number to PII data. As a result, it serves as a single gateway to stronger, simplified, and secure identity verification.

Faster Application Capture Using Auto-fill: According to the Built For Mars study referred to earlier in this article, it takes 24 to 45 clicks to open a challenger bank account in the UK. While significantly faster than incumbents, this could be improved further by auto-filling PII data. While auto-filling forms using social auth have existed for a while, in addition to consumer apprehensions around security and data privacy, the authenticity and cleanliness of data fetched are often questionable.

The recommended best practice is to auto-fill demographic and PII data from verified sources as part of identity verification, killing two birds with one stone. Auto-filling backed by a strong identity verification method reduces the time to complete an application significantly while delivering a high level of confidence in the authenticity of the data.

Prove Pre-fill™ can simultaneously solve application abandonment and security issues associated with consumer applications. In addition to reducing the friction in the form-filling process, it also mitigates identity fraud and minimizes the need for costly manual reviews.

Converge CIP, Auto-fill, and Fraud Checks on a Single Platform: Most customer onboarding processes are backed by a spaghetti of software tools and applications—each addressing specialized functions of identity verification, KYC, and fraud checks—resulting in redundancies and inefficiencies. This results in higher operational costs, negatively impacting CAC.

Rationalizing the onboarding application landscape and optimizing the onboarding tasks onto a single identity and fraud management platform delivers lower CAC apart from better agility and efficiency gains.

Passive but Stronger Authentication: Most challenger banks today rely on legacy 2FA practices for authentication, the most prevalent practice being SMS-based one-time-passcodes. With a rampant increase in identity takeover fraud of late, especially those involving SMS interception and SIM swaps, challenger banks should consider upgrading to stronger 2FA methods based on mobile-based authentication and behavioral biometrics. While both these methods present an opportunity to phase out SMS-based OTPs for 2FA completely, they could also be used to fortify an existing OTP-based 2FA process, where there is a risk of disrupting an existing customer journey.

Apart from reinforcing identity verification by validating the correlation between the device and the phone number, mobile auth and behavioral biometrics—by their very nature—are passive and silent, thereby increasing convenience and improving the overall user experience. The results are particularly pronounced in user logins, password resets, and financial transactions, where the risk of compromised ownership is high.

Prove’s Mobile Auth™ connects with mobile networks to verify that activity is coming from an expected device, authenticating customers without the need for easily compromised passwords or PINs. In addition, since it is built on core network infrastructure, it is a secure and frictionless method to strengthen a customer’s authentication flow, either as a replacement for OTPs or fortifying them.

With the acquisition of UnifyID, Prove now enables mobile behavioral biometrics technology. It is the only solution in the market that can definitively authenticate a person with a 1:1 match using a person’s behavior and movement.

Get in touch

The modern

way of proving identity

Trusted by 2500+ leading companies to reduce fraud and improve consumer

Keep reading

Read the article: Account Takeovers: The Silent Revenue Killer

Read the article: Account Takeovers: The Silent Revenue KillerAccount takeover (ATO) fraud is rapidly becoming one of the biggest threats facing digital marketplaces and gig platforms. Learn how ATO attacks work, why they are accelerating, the latest fraud trends and statistics, and how continuous identity verification helps organizations prevent account takeovers while protecting revenue, customer trust, and user experience.

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces Dry

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces DrySMS pumping fraud is silently increasing verification costs for digital marketplaces by exploiting OTP workflows. Explore how these attacks operate, why traditional SMS authentication is failing, and how proactive phone intelligence can prevent fraud before an SMS is sent.

Read the article: Prove and Baselayer Partner to Bring Real-Time Business Verification to ProveX

Read the article: Prove and Baselayer Partner to Bring Real-Time Business Verification to ProveXProve and Baselayer simplify business verification by combining trusted identity, real-time KYB intelligence, and seamless onboarding into a single workflow without requiring additional verification steps.

Trusted by 2000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.