What Goes Wrong for Insurers Who Don't Get Identity Right

Fraudsters are using customer information stolen from breaches and other schemes to target insurance companies via identity fraud.

.png)

It’s no secret that consumer data is “out there," being bought and sold on the dark web, and used regularly by bad actors for application fraud across the private and public sectors, including the insurance industry.

Identity theft has grown so rampant that it’s become a national conversation. President Biden made a point in his State of the Union address this year to mention that identity theft losses related to the distribution of funds during the pandemic will total billions of dollars. The White House is taking action and has since gone on to name a new chief prosecutor, Associate Deputy Attorney General Kevin Chambers, who describes the amount of data his team must sift through as “shocking.”

Of course, the problem is even larger than just pandemic-related losses. In the US:

- Someone becomes a victim of identity theft every 14 seconds.

- In 2020 alone, victims filed 2.2 million reports with the FTC.

- Some sources believe up to 33% of all Americans have been victims of identity theft.

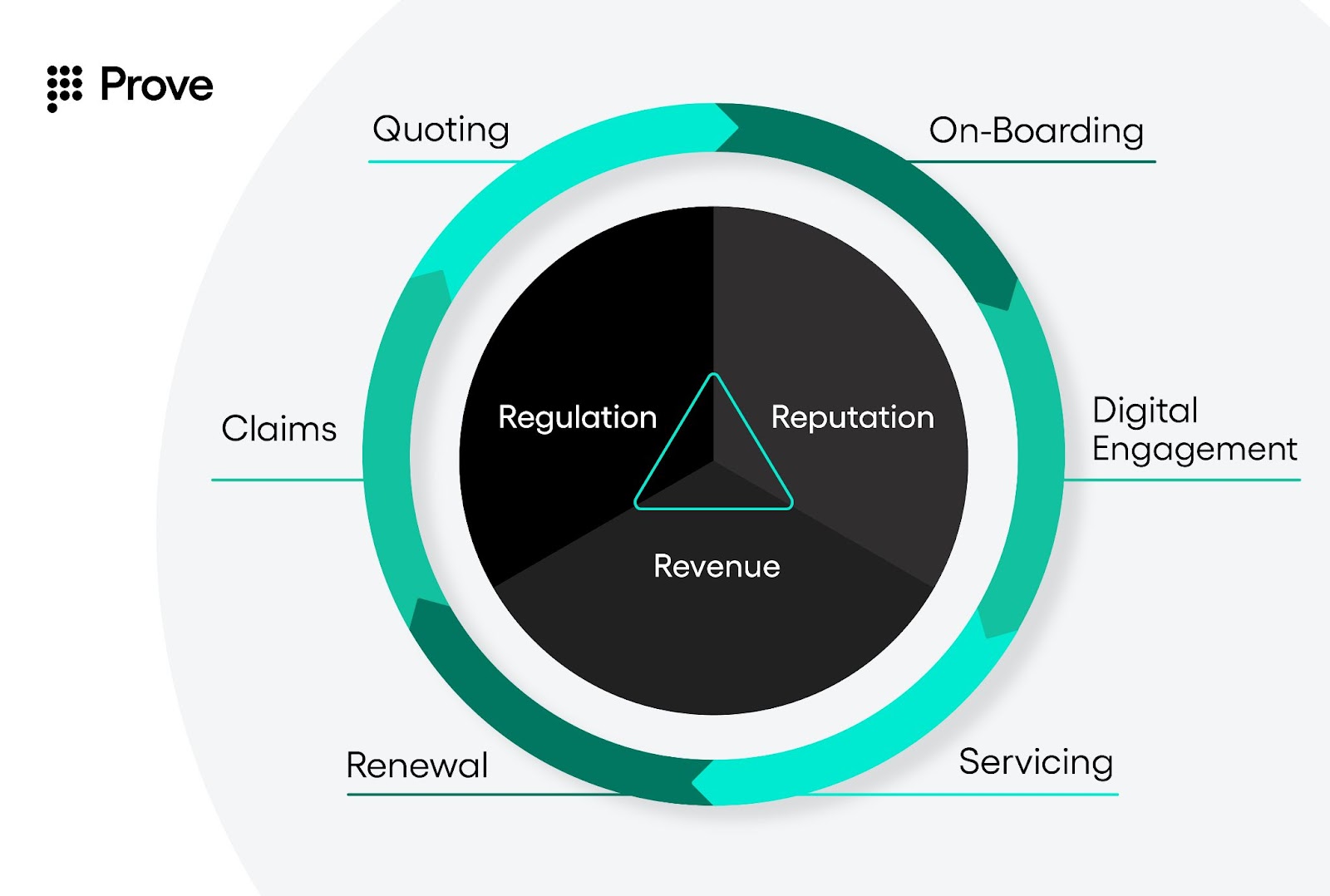

Increasingly, insurance companies are experiencing the true cost of fraud first-hand in the form of damaged reputations, class-action lawsuits, and increased scrutiny from regulators. In this article, we’ll cover the macro forces driving fraud, explore the most common forms of fraud targeting the insurance industry, and review the three things every insurance company should do to protect themselves and their customers from fraud.

What is going wrong?

Fraudsters are using customer information stolen from breaches and other schemes (keep reading for the specifics) to target insurance companies via identity fraud. Because the bad actors have customer data, they can easily pass most application flows that require data input to "fake" an identity. As a result, even some of the biggest companies are realizing that many insurance policies are opened under fictitious identities, leading to fraudulent claims down the road.

What fraud use cases should insurers be aware of?

Let's take a look at one important use case especially relevant to insurers: application fraud. Application fraud takes place when a fraudster uses false information to complete an onboarding flow.

In a recent high-profile case, fraudsters used basic consumer information to begin the quote process. The insurance company then auto-filled the application with additional customer information, including the victim’s driver’s license number, to streamline the process and accelerate onboarding. While this sounds like a good idea, it was actually a critical mistake. The fraudster “scraped” the new information that was auto-filled on the forms (including driver’s license numbers) and used the additional data to fraudulently apply for unemployment insurance under the victim’s name. By auto-filling forms with sensitive customer information BEFORE authenticating or verifying the user, the insurance company inadvertently helped criminals defraud victims. Lesson learned: identity proofing the user should be one of the first steps in any onboarding process.

What’s driving application fraud in the insurance industry?

Insurance companies have been making it easier for customers to obtain insurance products online in the last decade. While this is great news for legitimate customers, it also creates opportunities for bad actors.

In today’s digital-first environment, effective identity proofing is critical to every step of the insurance journey. By following best practices, insurance companies can increase revenue, protect their reputation, and prevent unnecessary regulatory scrutiny.

What can insurers do to stop the cycle of fraud?

Although banks have historically taken the hardest hit when it comes to fraud, insurers are far from immune. Today, fraudsters have learned that there’s big money in defrauding insurers and are leveraging application fraud at an unprecedented rate. To prevent fraud and protect their reputations, insurers must up-level their identity proofing.

To stop fraud, it’s important to get to the root of the problem. In the case of application fraud such as the example given above, the problem lies in the fact that the insurer’s application flow lacks the digital identity proofing capabilities necessary to provide a high level of assurance that the consumer is who they claim to be. Put simply, to build an application flow that prevents fraud, you need to know that you have the right person at the other end of the digital interaction. This assurance level is critical to the complete set of interactions that will follow.

Here are three steps every insurance company should take ASAP to improve their digital identity and security posture:

- Safeguard and accelerate onboarding flows with advanced account opening solutions such as Pre-Fill®: Prove Pre-Fill auto-fills online forms with verified consumer data from authoritative sources (with the consent of the user), authenticates consumer identities to thwart account opening fraud such as synthetic identity fraud, and offers users a faster, more secure, and consent-driven sign-up process.

- Embrace cryptographic authentication for seamless MFA: Cryptographic authentication (AKA key-based authentication) allows insurance companies to trust that the data asserted by users during authentication and verification events is true by leveraging the cryptographic key within a consumer’s mobile phone as the source of truth. Because it uses something that almost every adult consumer already has, cryptographic authentication is the most scalable but also the most accurate way of proving identity online today.

- Harness Prove’s three-step PRO check: Today, the best way to authenticate a user online is not with a password but rather by running a PRO check. If a user passes all 3 checks, you can feel confident that it really is them on the other side of a transaction.

What is a PRO check?

A PRO check is composed of the 3 checks companies should use to fortify their identity verification & authentication: Possession, Reputation, and Ownership:

- Possession answers the question: Is this customer in possession of the phone? Knowing that someone is in possession of a phone at the precise moment of a potential transaction helps identify someone regardless of the transaction channel and helps ensure the customer is indeed on the other end of an interaction.

- Reputation answers the question: Are there risky changes or suspicious behaviors associated with the phone number? Typically, people have had the same phone number for a long time and upgrade phones only every few years. Compare that to a burner phone, a phone that underwent a SIM swap, or a phone number that was just registered. These activities lower the reputation of the phone itself, which allows companies to flag the phone regardless of customer activity.

- Ownership answers the question: Is the customer associated with the phone number? It is crucial to associate a phone number with a person when confirming that the customer is in possession of the phone. Otherwise, the wrong person may be verified. This means knowing when a customer truly gets a new phone number or knowing that phone number is still associated with a person even if they switch carriers.

What are other ways that the insurance industry can protect itself against escalating rates of fraud?

While insurance companies who are proactive in leveraging the advanced identity technology described above will differentiate themselves by bettering customer experience and better protecting their customers, there are also important steps the industry must take as a whole to address rising rates of fraud. This year, the NAIC (National Association of Insurance Commissioners) created the Anti-Fraud Technology Working Group that is charged with reviewing and providing recommendations for the development of an Anti-Fraud Plan Repository. This repository will be used by insurers to create and store electronic fraud plans for distribution among various states and jurisdictions. The output of this working group and others focused on cybersecurity is expected towards the end of 2022 and should be a good start for an actionable plan.

Final Words

Insurance companies today must develop identity proofing technology that protects their customers from a wide range of fraud and accelerates onboarding to boost revenue. By leveraging Prove’s cryptographic authentication technology, insurance companies will be able to protect their industry’s reputation among the public and avoid unnecessary regulatory scrutiny. With Prove’s exceptionally simple API structure and skilled team of identity experts, integration is a simple and straightforward process.

Want to get identity right for your insurance company? Contact a Prove fraud expert today.

The modern

way of proving identity

Trusted by 2500+ leading companies to reduce fraud and improve consumer

Mary Ann Miller is the Fraud & Cybercrime Executive Advisor and VP of Client Experience at Prove. Mary Ann is a well-respected expert in the fraud and identity space who has been quoted by Sky News, TechCrunch, American Banker, USA Today, and others. Mary Ann was most recently Head of Fraud Strategy at Varo Bank, where she led the fraud strategy process for transitioning the fintech to a nationally chartered challenger bank. Prior to that, Mary Ann's held directorships and executive roles at well-known organizations such as USAA, PayPal, Lloyd's Banking Group, and other technology firms. She has also served on the US Federal Reserve Secure Payments Task Force and is a current member of the Federal Reserve’s Scams Definition and Classification Work Group.

Keep reading

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for Business

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for BusinessProve Pre-Fill® for Business provides a comprehensive solution for organizations that want to onboard businesses by delivering faster onboarding, a decrease in abandonment, and a reduction in fraud (relative to attack rate).

Read the article: Account Takeovers: The Silent Revenue Killer

Read the article: Account Takeovers: The Silent Revenue KillerAccount takeover (ATO) fraud is rapidly becoming one of the biggest threats facing digital marketplaces and gig platforms. Learn how ATO attacks work, why they are accelerating, the latest fraud trends and statistics, and how continuous identity verification helps organizations prevent account takeovers while protecting revenue, customer trust, and user experience.

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces Dry

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces DrySMS pumping fraud is silently increasing verification costs for digital marketplaces by exploiting OTP workflows. Explore how these attacks operate, why traditional SMS authentication is failing, and how proactive phone intelligence can prevent fraud before an SMS is sent.

Trusted by 2000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.