What is Check Fraud and How Can Banks Prevent It?

What is Check Fraud and How Can Banks Prevent It?

What is Check Fraud and How Can Banks Prevent It?

Check fraud is a type of financial crime that occurs when a perpetrator steals, alters, or forges a check to access someone else's funds. This type of fraud has been around for decades, but it has seen a significant increase in recent years, with a remarkable 385% surge since 2021.

This overview of check fraud, including methods to prevent it, is based on an American Banker webinar presented by Prove Fraud & Cybercrime Executive Advisor Mary Ann Miller and fraud expert Frank McKenna. It delves into the factors driving the spike in check fraud, its impact on customers, and the security measures that banks can take to mitigate this growing problem. For more information, you can watch the full webinar.

“Roughly 60% of check fraud is the result of onboarding someone that shouldn’t have been onboarded. Preventing the proliferation of fake accounts is the best way to stop check fraud.” - Mary Ann Miller, Cybercrime Executive Advisor

Wait, people still use checks?

With the growing popularity of digital payments, checks and check fraud can appear rather antiquated. The reality, however, is that even with Zelle, PayPal, Cash App, and other P2P services, many consumers still prefer to pay their bills or send money “the old-fashioned way”– that is, writing a check and mailing it to the payee. Unfortunately, the enduring popularity of checks gives scammers a golden opportunity to commit check fraud.

In short, although paper check usage is down from its heyday, checks are still in circulation, and fraud capitalizing on this method of payment is on the rise.

How does check fraud work?

To hide their identities, criminals often create numerous fake bank accounts, known as “mule accounts.” This can be accomplished using either stolen identity information from real individuals or combining information from multiple sources to create a new fictional identity (known as synthetic identity). Due to the abundance of personal data leaked from data breaches and available for purchase on the dark web, this step is fairly easy.

After the fraudster has established multiple checking accounts under assumed identities, they obtain checks either by purchasing them on the dark web or by stealing them from mailboxes. Organized criminals will either “fish” envelopes out of post boxes or steal the keys necessary to open the post boxes. Tragically, this step has resulted in an alarming spike in violence against mail carriers around the country.

Finally, the criminal either “washes” the checks and addresses them to the various fake identities that they have created or simply adds a new payee. They then deposit the checks using the ATM, mobile deposit, or even a branch of the bank. In just a matter of minutes, the criminal can walk away with thousands of stolen dollars in their pocket.

What are the different types of check fraud?

Forged signatures: This is when someone signs a check using someone else's name without consent. This can be done by physically altering a legitimate check or by creating a fake check with a forged signature.

Alteration of checks: This is when someone changes the information on a legitimate check, such as the amount or payee, to steal money.

Check kiting: This is a fraudulent practice where someone writes a check from one bank account to another, knowing that there are insufficient funds in the account to cover the check. They then deposit the check into the second account and withdraw the funds before the check bounces.

Check washing: This is when someone alters the payee or amount on a check by removing the ink with chemicals or other methods and then rewrites the check for a larger amount or to a different person.

Is check fraud a serious crime?

Yes, check fraud is a serious crime that can result in jail time. Depending on the severity of the offense and the amount of money stolen, the penalties for check fraud can include fines, probation, community service, and imprisonment. In some cases, the offender may be sentenced to several years in prison. Of course, the penalties vary depending on the jurisdiction and the circumstances of the case. That being said, many cases, unfortunately, go unprosecuted because of just how common the crime is.

What is the impact of check fraud on victims?

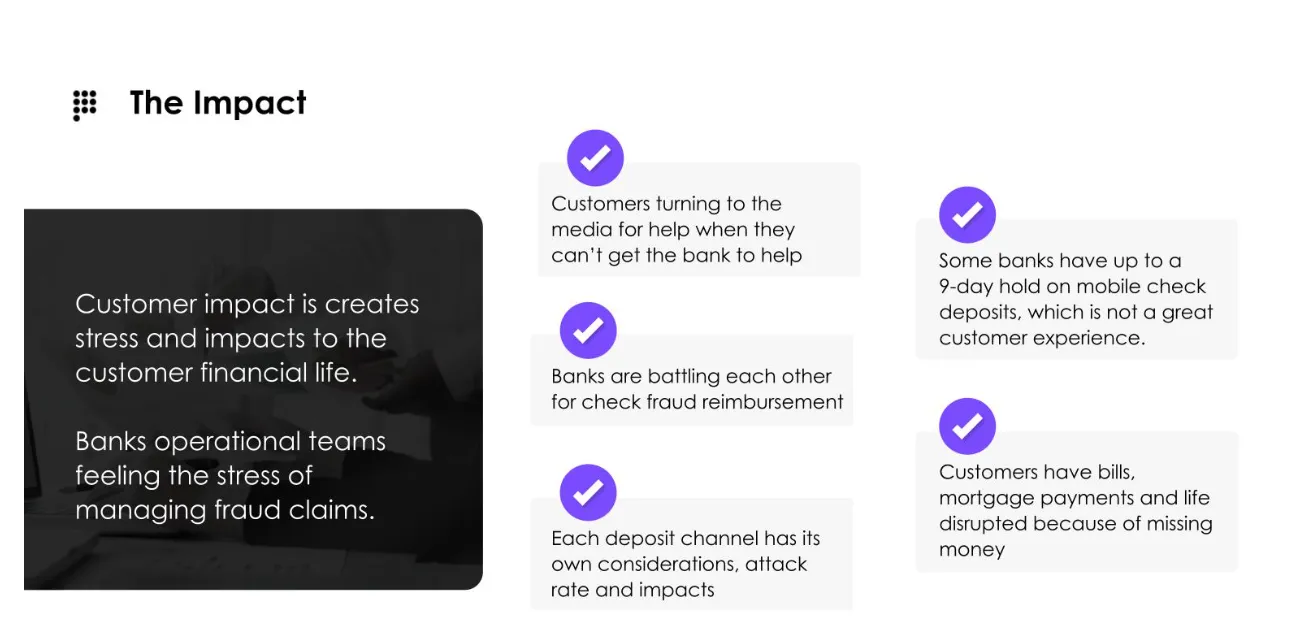

Check fraud can have a significant impact on customers' financial well-being. First, the check they sent to pay their bills or send money to a loved one never reaches its destination. If they are paying the electric bill and the check gets intercepted, for instance, they might have their power turned off

After a victim’s check is intercepted and altered, the victim will likely be hit with an overdraft fee from their bank. In the worst-case scenario, the bank may even close the victim’s account for bouncing a check. Although customers can work with their bank’s fraud department to avoid paying these fees and unfreeze their accounts, this process can be stressful and time-consuming.

Finally, legitimate customers have to deal with the security measures many banks have put in place to slow down check fraud. For example, many banks have resorted to placing a staggering nine-day hold on all mobile deposits, greatly impacting legitimate customers who want speedy access to their funds. If you’re in the financial services industry, keep scrolling to learn a better way to slow down check fraud without negatively impacting your customer.

What is the impact of check fraud on banks?

It’s difficult to overstate the current impact of check fraud on banks. Although check usage has been declining for over two decades, check deposit fraud is increasing. In fact, according to some estimates, check deposit fraud has increased by a staggering 385% between 2021 and 2022. Although it garners less attention, check fraud losses are bigger than both Zelle fraud and credit card fraud.

Check fraud puts a significant strain on banking operations. Considering that the back offices of many banks are flooded with altered checks that need review, it’s no wonder that fraud departments are running through their budgets faster than anticipated, and customers are paying the price in long wait times for reimbursements.

To make matters worse, fraud begets fraud and we’re watching in real time as the check fraud crisis results in a secondary crisis: first-party check fraud. This is when a consumer claims their check was stolen and forged but it really wasn’t.

What should banks do to mitigate check fraud?

There are several measures that banks can take to mitigate the risks of check fraud. Here are five areas that banks should focus on ASAP:

- Incorporate Identity Verification in Onboarding Technology: Fraudsters rely on having access to multiple mule or synthetic bank accounts to steal funds via check fraud without a trace. Many of these accounts are established with the help of bots. Stopping the proliferation of fake bank accounts by up-leveling digital identity technology is critical. With the proper digital identity-proofing checks in place, a consumer must verify their identity through a mobile phone before being allowed to open an account. Implementing solutions such as Prove Identity™ is critical because fraudsters are always on the search for institutions that don't have proper digital identity-proofing in place and they even compare notes on Telegram and Reddit to let other criminals know where they've seen success or failure.

- Use a Risk Behavioral Model: Establishing trust takes time which is why implementing a risk behavioral model makes a lot of sense. Without a risk behavioral model in place, the bank either trusts the user or doesn’t. With a risk behavioral model, however, the bank can limit high-risk transactions until the consumer has proven themselves trustworthy over a set amount of time, perhaps 60-90 days.

- Build Trust Files: Banks can start collecting data to build a trust file that can predict whether a check is legitimate or fraudulent. For instance, a $50 check to a local utility shouldn’t be flagged but a $10,00 check sent to a newly created bank account should be flagged for review. This is often referred to as payee analysis and out-of-pattern altered checks.

- Reconsider Hold Strategies: Hold strategies can limit the risks of check fraud by increasing the amount of time it takes for a bank to clear a check. However, increasing the hold times is not ideal for legitimate customers as they now have to wait longer and longer to access their money. To make matters worse, hold strategies will never solve check fraud entirely. Instead, it just buys some time. Banks should try to avoid hold strategies and instead focus on improving onboarding controls.

- Embrace Emerging Technologies: Although many banks are reluctant to invest funds into preventing check fraud given that check usage is on the decline, new technologies are emerging that may be worth their price. Artificial intelligence, for instance, can visually inspect checks, enabling banks to readily identify alterations, counterfeiting, mismatched signatures, etc.

Bonus tip: investing in driver's license scanning and fingerprinting technology can give bank tellers the tools they need to become fraud fighters.

“Today, there are more ways than ever before to cash a check. To stop check fraud, we must fortify everything from bill payments to mobile deposits, ATMs, and bank branches.” - Mary Ann Miller, Cybercrime Executive Advisor

Conclusion

Check fraud is a growing problem that is causing significant losses for customers and banks alike. Banks must take steps to mitigate this problem by investing in an onboarding technology that incorporates identity verification, using risk behavioral models, building trust files, considering alternatives to hold strategies, and leveraging emerging technologies.

Investment in check fraud detection technology is often difficult because many people consider paper checks a dying form of payment despite their enduring popularity. To solve this problem, however, fraud experts can pivot to focusing on identity proofing (front-end controls) that solve a variety of fraud vectors, including but not limited to check fraud.

The modern

way of proving identity

Trusted by 2500+ leading companies to reduce fraud and improve consumer

Keep reading

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for Business

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for BusinessProve Pre-Fill® for Business provides a comprehensive solution for organizations that want to onboard businesses by delivering faster onboarding, a decrease in abandonment, and a reduction in fraud (relative to attack rate).

Read the article: Account Takeovers: The Silent Revenue Killer

Read the article: Account Takeovers: The Silent Revenue KillerAccount takeover (ATO) fraud is rapidly becoming one of the biggest threats facing digital marketplaces and gig platforms. Learn how ATO attacks work, why they are accelerating, the latest fraud trends and statistics, and how continuous identity verification helps organizations prevent account takeovers while protecting revenue, customer trust, and user experience.

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces Dry

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces DrySMS pumping fraud is silently increasing verification costs for digital marketplaces by exploiting OTP workflows. Explore how these attacks operate, why traditional SMS authentication is failing, and how proactive phone intelligence can prevent fraud before an SMS is sent.

Trusted by 2000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.