Anyone Can Lend! With a Customer Base, Data, & Ability to Create Immersive Experiences

People often ask – what is the most significant driver for FinTech innovation? Is it the reduced cost of running a startup, banks offering bad service, or the democratization of tools & software?

People often ask – what is the most significant driver for FinTech innovation? Is it the reduced cost of running a startup, banks offering bad service, or the democratization of tools & software? Is it the ease of technology creation (supply-side dynamics with open source, cloud, etc.) or ease of technology consumption (demand-side dynamics like smartphone + internet penetration, cost of data, etc.)?

We discussed and debated. We narrowed it down to one thing – mobility-driven customer expectations, wherein everything should happen in four clicks on the phone. Everything else (other drivers of FinTech) is to satisfy that demand.

Ask yourself about the one big factor that led to this change. The mobile experience in other industries like transportation (Uber/Ola), hotels (Expedia/MakeMyTrip), and e-commerce makes people demand similar experiences in FinServ. Who is best positioned to satisfy the need in the long run if this is the case? Is it only the FinTechs and their bank partners, or does this truly open the market to new players?

One may argue that some of the finest FinServ experiences are built by commerce or non-banking/non-FinTech companies (Starbucks, Alipay, WeChat Pay, etc.). However, that may not be a secular and scalable trend. What we do believe, though, is that there is an opportunity to democratize the delivery of financial services.

Let’s take a look at the payments sector: payments have always been the last part (or one of the last parts) of the commerce journey. The best experiences are those that can’t be seen or felt (Uber or Amazon Go). Instead, their technology creates immersive experiences. Over the last few years, I have spent some time in China and have witnessed these immersive experiences with the convergence of enabling technologies that the Chinese companies have built.

What’s happening in China is the playbook for FinTech. My favorite example is Alipay. The average amount that a Shanghainese Alipay user paid for food using the Alipay wallet runs in thousands of dollars – this demonstrates the immersive nature of the platform to handle food and their distribution channels, whether online or offline (from streetside hawkers to supermarkets to restaurants). It’s a much more extensive data play that uses location, preferences, buying patterns, targeted offers, personalization, etc., to offer a broader set of financial and non-financial offerings.

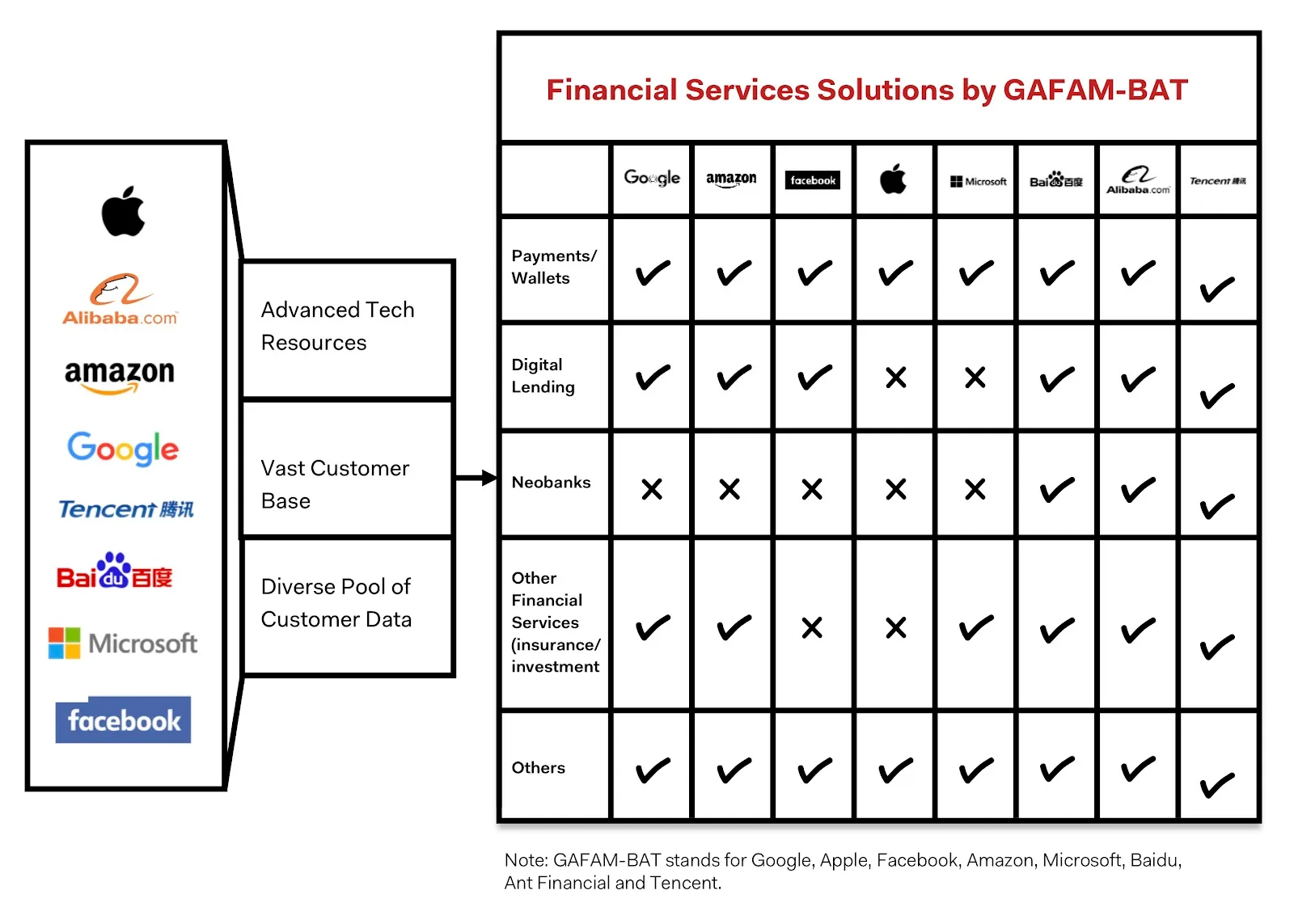

Because of all the above reasons, would you believe me if I said anybody with a vast customer base & data could lend? Anybody = especially internet & consumer technology companies. ‘Lending’ is a generalization, but it could be any financial service for that matter – payments, lending, and perhaps even insurance. A player like Amazon or Grab enhances the consumption of goods/services by doing just that. If you aren’t sold on my hypothesis yet, let’s check out some examples and objectively assess this hypothesis:

- In January 2012, Amazon started something that shocked the financial world. Amazon started offering small business loans in amounts from $1k to $750k, a total of more than $3 billion in loan originations as of July 2017. The past couple of years has seen many non-FinServ players partnering with banks/FIs and developing lending offerings across consumers, small businesses, working capital, and microcredit products. Leading ride-sharing startups such as Grab, Ola, and GO-JEK have launched microcredit offerings for driver-partners and other micro & small business customers.

- Xiaomi launched microloan services for MIUI users with $1.4 billion in loan origination as of November 2017. It also launched MI Loans, a mobile app-based lending service in China. Recently, it launched a microlending product in India for salaried professionals in partnership with KrazyBee.

- Flipkart has applied for an NBFC license in India to focus on consumer lending. It is expected to take a hybrid approach by owning a good chunk of the loan book and creating a curated marketplace for lenders.

- Shopify launched Shopify Capital, a cash-advance service for its merchants in the US.

- Intuit launched a loan offering called ‘QuickBooks Capital’ for small business clients. Clients can avail up to $35,000 for six months, right from inside their bookkeeping software.

- Grab partnered with Credit Saison to offer microcredit to Grab drivers and businesses through their GrabPay service with $700 million in loan originations YTD. Grab has also partnered with Indonesian bank BNI to provide micro-lending services to its micro & small business customers in the culinary industry that are registered partners of its Go-Food service.

- WhatsApp in India started pilot testing payments in its messaging & calling app, which has more than 250 million highly engaged users.

FinServ is one space that touches every business segment and individual. So I’m making a case for internet & consumer technology companies here in the FinServ space. If the customer base, their information, transaction data, technical prowess, and above all, building great immersive experiences is what is required, who has the best chance of winning?

All is not well for such endeavors; not all initiatives in this regard have been successful. Tech companies have to learn ‘Fin’ to make FinTech work. Despite some early failures, there is a massive opportunity for value creation by TechFins. Tech giants are beginning to use their tech brainpower, user base, and data to offer superior financial services experiences. Alipay and WeChat are leading the way and, in the process, are building some interesting tech infrastructure that can revolutionize FinServ back-end operations.

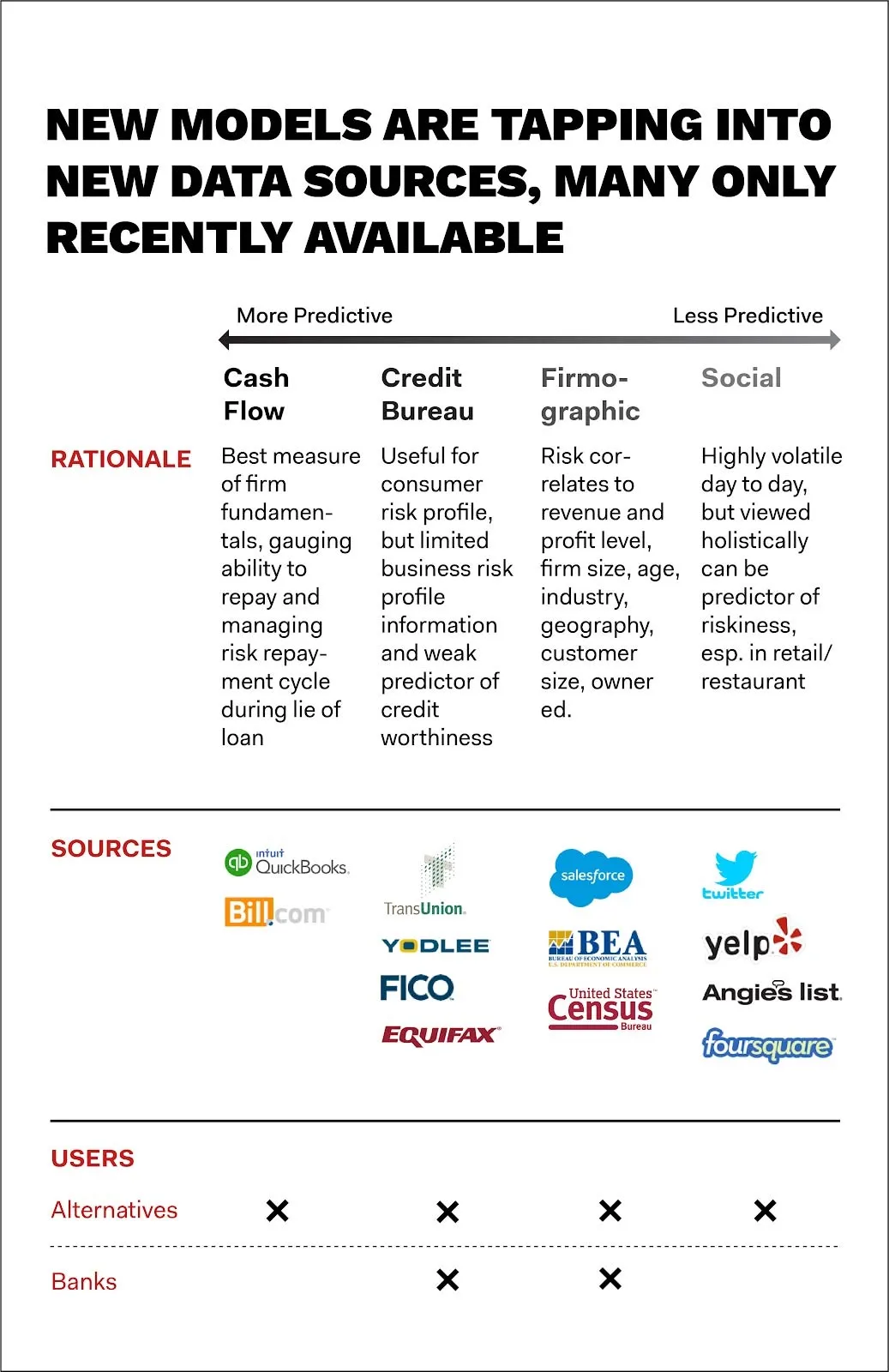

It fits in with segment-specific trends as well. For example, lending has become a pure data play (transactional data & past behavior).

Let me point you to another big connection: PSD2 in Europe. It is taking shape in the form of Open Banking. We were talking to the CTO of a European bank who has built the Open Banking platform as well as the APIs – it turns out he now wants to work with the TechFins.

I think in five years, we may or may not call this industry FinTech. Maybe the overuse of the term FinTech will go away. It will get consumed by industries as a layer – invisible payments, data-driven, API-led lending, and so on. Look at it from the perspective of a customer (four-click experiences), TechFin (data & captive audience play), Open Banking, or any other perspective – it just makes so much sense. I think the time has come: anyone can lend or sell insurance.

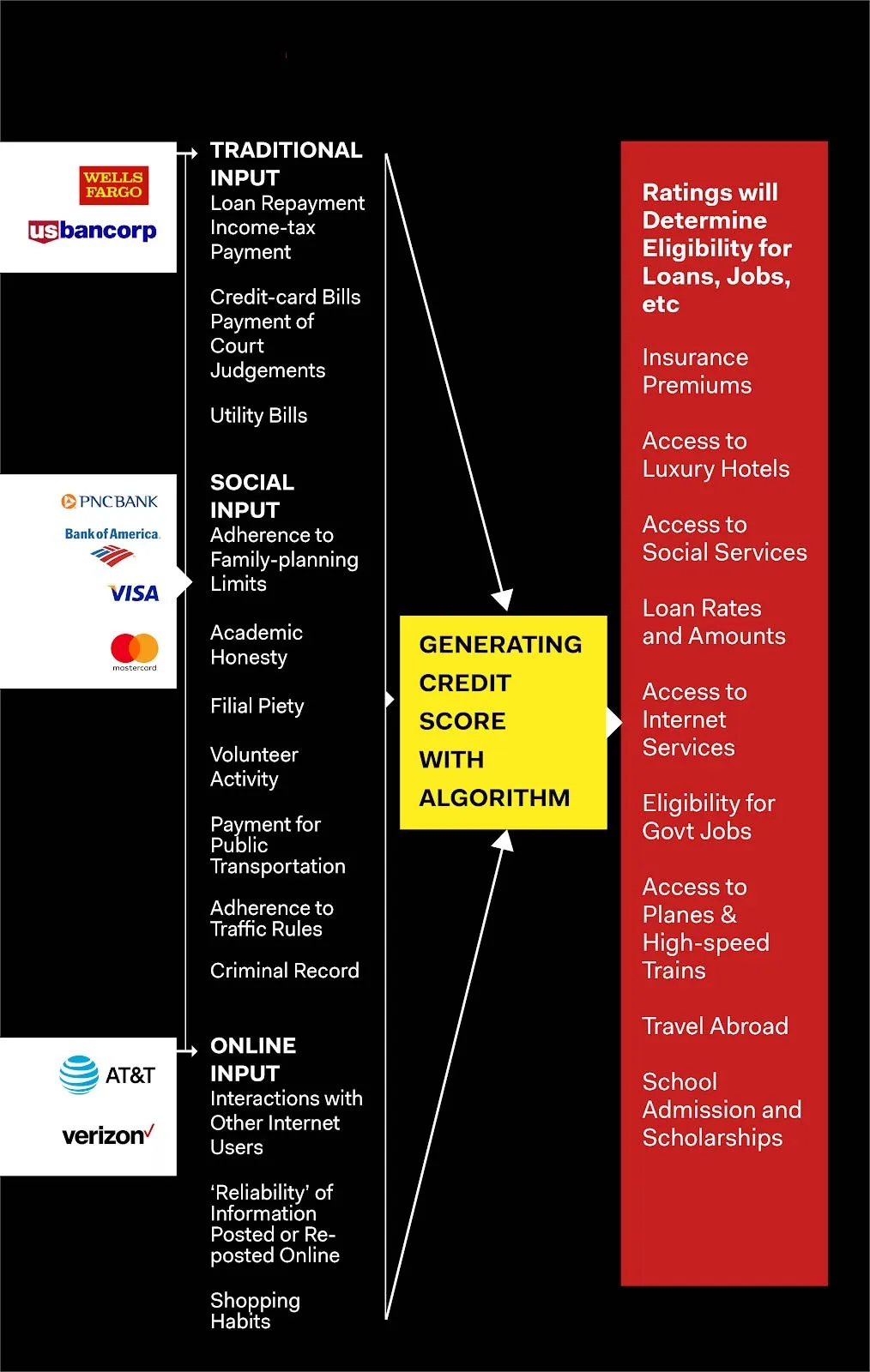

PS: I’ll leave you with one last thought: Better underwriting – There is a school of thought that believes some of these TechFins can do a better job at underwriting. Alibaba and its subsidiaries (Alipay, Sesame Credit) have created a model where identity, authentication, credit score, job eligibility, admissions, and access are all colliding to make way for the ‘social score.’ The possibilities are endless.

To learn about Prove’s identity solutions and how to accelerate revenue while mitigating fraud, schedule a demo today.

The modern

way of proving identity

Trusted by 2500+ leading companies to reduce fraud and improve consumer

Keep reading

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for Business

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for BusinessProve Pre-Fill® for Business provides a comprehensive solution for organizations that want to onboard businesses by delivering faster onboarding, a decrease in abandonment, and a reduction in fraud (relative to attack rate).

Read the article: Account Takeovers: The Silent Revenue Killer

Read the article: Account Takeovers: The Silent Revenue KillerAccount takeover (ATO) fraud is rapidly becoming one of the biggest threats facing digital marketplaces and gig platforms. Learn how ATO attacks work, why they are accelerating, the latest fraud trends and statistics, and how continuous identity verification helps organizations prevent account takeovers while protecting revenue, customer trust, and user experience.

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces Dry

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces DrySMS pumping fraud is silently increasing verification costs for digital marketplaces by exploiting OTP workflows. Explore how these attacks operate, why traditional SMS authentication is failing, and how proactive phone intelligence can prevent fraud before an SMS is sent.

Trusted by 2000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.