Banks and Apple Pay: The Love-Hate Relationship

The widely adopted Apple Pay is a controversial topic that has not been left aside whenever mobile payments solutions are discussed.

The widely adopted Apple Pay is a controversial topic that has not been left aside whenever mobile payments solutions are discussed. Undoubtedly, Apple Pay can be considered a game-changer in pushing ahead contactless payments. However, there are different sides to the story depending on the party. The consumer perception of Apple Pay may differ from that of the banking industry that is actively deploying the solution since the moment it was launched. Along with all the advantages that Apple Pay offers to its users, the banks absorb the costs of convenience. Banks are now facing the controversial question of consumer demand and hidden rocks it has to cover on the other. That tendency creates love-hate relationships between the banking industry and a payment solution.

To have a holistic view of what drives those relationships and why banks are forced to get along with Apple Pay, let us start from the beginning: how it became possible for mobile payments solutions to take over other methods, and then turn to Apple Pay’s dilemma.

Smartphone Revolution

Over the past few years, the smartphone revolution brought consumers a new way of shopping and payments. As mobile becomes a massive part of consumers’ lives, they turn to their phones to get most things done. There is a certain shift in expectations from mobile technology and mobile payments leaders. According to the Pew Research Center study US Smartphone Use in 2015, 64% of American adults own a smartphone. Below is a chart provided by Pew Research Center on the ways smartphone owners use their devices.

As we can see, smartphones serve a wide range of needs. For example, an impressive 57% of smartphone users using online banking drove banks online and shifted the industry’s focus from branches to improve the online experience. To stay relevant, businesses have to follow customers and improve the channels preferred by them.

A different study by VeriFone and Wakefield Research titled The Path of Payments 2015, suggests that more than half of the surveyed consumers feel the need for merchants to adopt mobile payments.

However, the mobile revolution brought an explosion of online life and fostered a wave of technologies that utilize the mobility of our devices and new behavioral trends—mobile consumerism. The rise of mobile device usage led industries to cater to consumers via mobile applications and accept payments through mobile devices. Mobile payments options are now a crucial part of any business as a revenue-driving solution.

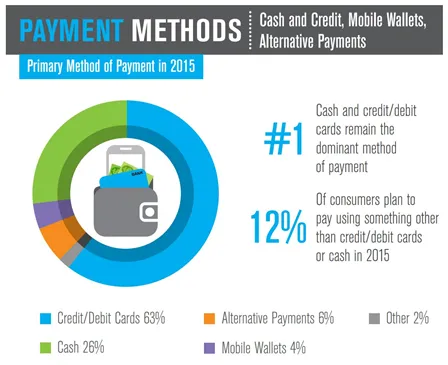

The Path of Payments 2015 also indicated that mobile wallets accounted for about 4% of the payments market for in-store US retail transactions.

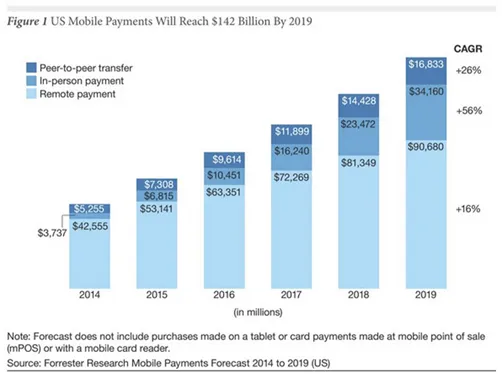

However, the overall industry of mobile payments is projected to grow, with remote payments accounting for the biggest part of all payments volume. CIO published the following chart describing the tendency:

Mobile payments are here to stay. We often hear about Apple Pay, Samsung Pay, Google Wallet, Android Pay, CurrentC, etc. But, for now, we will focus on Apple Pay. Soon after Apple Pay was launched, the service accounted for 1% of digital payment dollars while Google Wallet accounted for 4%, according to an article by The Guardian citing ITG Investment Research.

Merchants, Consumers, and Apple Pay

Launched in the US almost a year ago, Apple Pay supports credit and debit cards from the three major payment networks, American Express, MasterCard, and Visa, issued by 532 US banks. Since then, leading payment solution providers and terminal suppliers such as Adyen, Authorize.Net, Bank of America Merchant Services, Braintree, CyberSource, Chase Paymentech, First Data, Heartland Payment Systems, iMobile3, NCR, Oracle’s Micros, Stripe, TSYS, and VeriFone, among others, are working to bring merchants in stores and apps the ability to easily, securely and privately accept payments using Apple Pay.

For the sake of understanding the scale, figures provided by The Guardian on the number of Apple Pay accounts opened since the launch by the end of 2014 are worth sharing. JP Morgan Chase said that more than one million customers had added debit and credit cards to Apple’s service. In contrast, Bank of America has previously said 800,000 people had added 1.1M cards by the end of 2014—almost certainly making it the predominant mobile payment method in the US, displacing Google Wallet.

With a significant potential of the mobile payments industry and growth projections, Apple Pay remains one of the rare types of payments made at the POS. According to the results of the research on 100 US retailers reported by The Guardian, while some of the top US retailers said they use and like the mobile payment system, fewer than a quarter of the retailers said they accept Apple Pay, and nearly two-thirds said they would not be accepting it this year. Furthermore, out of 100 companies surveyed, only four reported plans to accept Apple Pay next year.

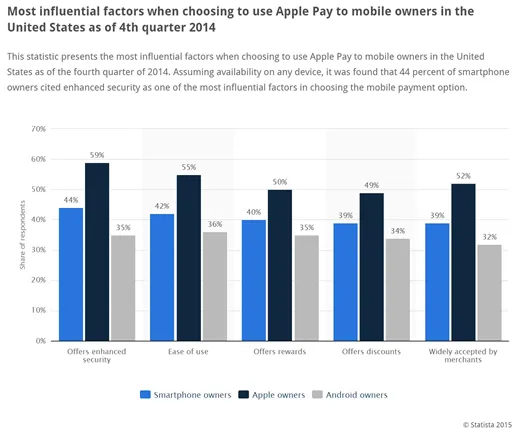

There are always pros and cons associated with any product or service; Apple Pay is no exception. The data provided by Statistical Portal demonstrated that among mobile device owners, the main reasons to use Apple Pay are enhanced security, ease of use, rewards, discounts, and wide acceptance by merchants. The percentage varies among different types of mobile devices. However, the range is between 32% and 59%, which is still high.

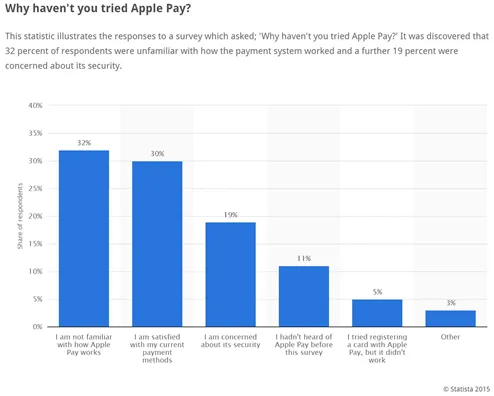

Along with the reasons to use Apple Pay, consumers are also not favoring this payment solution. Among the most common reasons people didn’t try Apple Pay are the unfamiliarity with the way it works (surprising? 32%), satisfaction with the current payment method (30%), and concerns about security (19%). It is also interesting that 11% have never heard of Apple Pay before the survey.

Speaking of security, the third main concern among the reasons not to use Apple Pay, we may now move to the banking industry, where that particular consumer concern has its monetary effect. In 2014, 40% of all financial fraud was credit card fraud, with 10% of Americans being victims of that particular type. Worldwide, the total amount of credit card fraud in dollars was $5.55 billion. In fact, in 10% of cases, the initial point of contact for fraud was a phone.

Banks and Apple Pay

The pros and cons consumers may see in Apple Pay are not necessarily the same for banks. The aspects and sides of the solutions banks are dealing with and implementing are different from those for the user.

One of the issues banks are facing with Apple Pay is security. This year, The Guardian published an article named Apple Pay: a new frontier for scammers. As stated in the article, the wave of fraudulent transactions through Apple Pay was surprising for banks rushing to stem the tide. Criminals in the US started using Apple Pay to purchase high-value goods (especially from Apple) using stolen identities and credit card details. As quoted in the article, mobile payments specialist who is a consultant to US finance groups, Cherian Abraham, said, At this point, every issuer (bank) in Apple Pay has seen significant ongoing provisioning fraud via customer account takeover. He also added that in some cases, fraudsters are calling the (bank’s) call center themselves to ‘alert them to a trip out of town’ so that fraud rules looking for transaction anomalies (such as a customer living in California and transacting in Miami) do not trip up (as) fraudulent transactions.

Forbes highlighted another reason; the credit card issuers (important note: those are banks responsible for paying that charge) are paying about 0.15% of an Apple Pay purchase as a guarantee by Apple that a tokenized and biometrically verified transaction is good. That cost is difficult to pass down to their customers, so the incentive for the credit card companies to promote Apple Pay is not significant. They are doing it, but grudgingly, as stated in the article.

One of the international examples of banking resisting Apple Pay is Australia. According to TechRadar, the issue is that the US banks generally make about $1 of profit for every $100 spent, so sharing 15 cents isn't that big a deal. However, in Australia, banks only make about 50c per $100, so giving up 30% of their profit to Apple is a sticking point. What makes things even more problematic is that the Reserve Bank in Australia wants to drive down that 50 cents per $100 down to about 30 cents, which would further erode their profits.

A recent survey conducted earlier in 2015 by CAN Capital on 1,125 small businesses called Adapting to Technology leads to the next reason, which may not be as strongly related to banks. Still, it affects them as account holders and financial service providers. Only 13% of small businesses accept mobile payments (including Apple Pay). A significant number—87% of small businesses—are not even accepting mobile payments. Low adoption of mobile payments technology among small businesses is one of the inhibitors for the banks to promote the service.

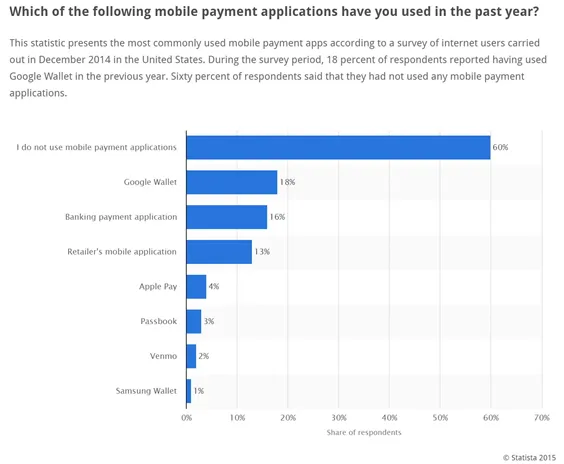

The low adoption rate is related not only to the small businesses. According to Statistical Portal, shortly after Apple Pay’s launch, Apple Pay was being used only by 4% of the surveyed.

Surprisingly, 60% of respondents do not use mobile payment applications. Even though figures of different sources may vary, they indicate a lower adoption rate for Apple Pay than other options, especially the 16% of users drawn to banking payment applications.

However, particular statistics of the current condition are not a reason for banks to bail on Apple Pay and mobile payments options. According to the same source, millennials (39%), Gen X (33%), baby boomers (19%), and mature (7%) are very interested in in-person mobile payments via tapping a receiver instead of traditional cash or payment cards as of February 2015.

The implication here is that even though adopting a particular service (such as Apple Pay) may be slow and low; there is a clear interest stemming from millennials and Gen X to use newer services instead of traditional payment options.

One of the reasons, along with those mentioned, is that Wal-Mart and 18 of the other top retailers surveyed by The Guardian are part of a coalition challenging Apple Pay with a mobile wallet called CurrentC. Retailers participating in CurrentC will not be allowed to accept any other mobile wallet until 2016, according to a senior official at MCX, the company operating CurrentC. For that reason alone, 19 of the NRF’s top 100 retailers will not be able to accept Apple Pay before the end of the year, although three of them said they plan to accept Apple Pay by early 2016.

Regardless of the downsides and low adoption pace of Apple Pay, according to the FT, the attraction for banks in partnering with Apple is the potential for more card transactions, earning them more revenue, even if they have to give up a small percentage to the tech group. Jeremy Nicholds, Executive Director of Mobile at Visa Europe, said, Contactless mobile phone payments are a driver of incremental transactions, creating an extra volume of revenue for banks, of which a share is passing through to Apple.

Conclusion

Along with other mobile payments options, Apple Pay confidently marches to the market, winning more and more payments to manage. Whether merchants or card issuers want it or not, mobile payments are here to stay and evolve to eliminate the flaws of existing options. As mentioned before, there are always pros and cons related to the product or service. Moreover, they are different depending on whether you are a consumer, a retailer or a financial services provider.

Modern customers are eager to try new options and adopt mobile payments at a more or less fast pace. Therefore, industries catering to customers’ needs have to adapt to the channels preferred by them. However, the emerging mobile payments market has its own issues forced onto banking and merchants. Even if the banking industry has to deal with higher risks and costs associated with mobile payment solution flaws, issuers have to follow the customer’s preferred channels to stay relevant and provide convenient services. Love-hate relationships between payments solutions providers and the conservative banking industry will always remain the same until there is a consensus on solving issues related to mobile payments.

To learn about Prove’s identity solutions and how to accelerate revenue while mitigating fraud, schedule a demo today.

The modern

way of proving identity

Trusted by 2500+ leading companies to reduce fraud and improve consumer

Keep reading

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for Business

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for BusinessProve Pre-Fill® for Business provides a comprehensive solution for organizations that want to onboard businesses by delivering faster onboarding, a decrease in abandonment, and a reduction in fraud (relative to attack rate).

Read the article: Account Takeovers: The Silent Revenue Killer

Read the article: Account Takeovers: The Silent Revenue KillerAccount takeover (ATO) fraud is rapidly becoming one of the biggest threats facing digital marketplaces and gig platforms. Learn how ATO attacks work, why they are accelerating, the latest fraud trends and statistics, and how continuous identity verification helps organizations prevent account takeovers while protecting revenue, customer trust, and user experience.

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces Dry

Read the article: The Silent Drain: How SMS Pumping Is Bleeding Digital Marketplaces DrySMS pumping fraud is silently increasing verification costs for digital marketplaces by exploiting OTP workflows. Explore how these attacks operate, why traditional SMS authentication is failing, and how proactive phone intelligence can prevent fraud before an SMS is sent.

Trusted by 2,000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.